Parties to a sales contract will usually agree on the obvious details of a sales transaction—the nature of goods, the price, and the delivery time, as discussed in the next chapter. But there are two other issues of importance lurking in the background of every sale:

- When does the title pass to the buyer? This question arises more in cases involving third parties, such as creditors and tax collectors. For instance, a creditor of the seller will not be allowed to take possession of goods in the seller’s warehouse if the title has already passed to the buyer.

- If goods are damaged or destroyed, who must bear the loss? The answer has obvious financial significance to both parties. If the seller must bear the loss, then in most cases he must pay damages or send the buyer another shipment of goods. A buyer who bears the loss must pay for the goods even though they are unusable. In the absence of a prior agreement, loss can trigger litigation between the parties.

Transfer of Title

Why It Is Important When Title Shifts

There are three reasons why it is important when title shifts from seller to buyer—that is, when the buyer gets title.

It Affects Whether a Sale Has Occurred

First, a sale cannot occur without a shift in title. You will recall that a sale is defined by the Uniform Commercial Code (UCC) as a “transfer of title from seller to buyer for a price.” Thus if there is no shift of title, there is no sale. And there are several consequences to there being no sale, one of which is— concerning a merchant-seller—that no implied warranty of merchantability arises. (Again, as discussed in the previous section, an implied warranty provides that when a merchant-seller sells goods, the goods are suitable for the ordinary purpose for which such goods are used.) In a lease, of course, title remains with the lessor.

Creditors’ Rights

Second, title is important because it determines whether creditors may take the goods. If Creditor has a right to seize Debtor’s goods to satisfy a judgment or because the parties have a security agreement (giving Creditor the right to repossess Debtor’s goods), obviously it won’t do at all for Creditor to seize goods when Debtor doesn’t have title to them—they are somebody else’s goods, and seizing them would be conversion, a tort (the civil equivalent of a theft offense).

Insurable Interest

Third, title is related to who has an insurable interest. A buyer cannot legally obtain insurance unless he has an insurable interest in the goods. Without an insurable interest, the insurance contract would be an illegal gambling contract. For example, if you attempt to take out insurance on a ship with which you have no connection, hoping to recover a large sum if it sinks, the courts will construe the contract as a wager you have made with the insurance company that the ship is not seaworthy, and they will refuse to enforce it if the ship should sink and you try to collect. Thus this question arises: under the UCC, at what point does the buyer acquire an insurable interest in the goods? Certainly a person has insurable interest if she has title, but the UCC allows a person to have insurable interest with less than full title. The argument here is often between two insurance companies, each denying that its insured had insurable interest as to make it liable.

Goods Identified to the Contract

The Identification Issue

The UCC at Section 2-401 provides that “title to goods cannot pass under a contract for sale prior to their identification to the contract.” (In a lease, of course, title to the leased goods does not pass at all, only the right to possession and use for some time in return for consideration.) Uniform Commercial Code, Section 2A-103(1)(j). So identification to the contract has to happen before title can shift. Identification to the contract here means that the seller in one way or another picks the goods to be sold out of the mass of inventory so that they can be delivered or held for the buyer.

Article 67 of the CISG says the same thing: “[T]he risk does not pass to the buyer until the goods are clearly identified to the contract, whether by markings on the goods, by shipping documents, by notice given to the buyer or otherwise.”

When are goods “identified”? There are two possibilities as to when identification happens.

Parties May Agree

Section 2-501(1) of the UCC says “identification can be made at any time and in any manner explicated agreed to by the parties.”

UCC Default Position

If the parties do not agree on when identification happens, the UCC default kicks in. Section 2-501(1) of the UCC says identification occurs

- when the contract is made if it is for the sale of goods already existing and identified;

- if the contract is for the sale of future goods other than those described in paragraph 3 below, when goods are shipped, marked, or otherwise identified by the seller as goods to which the contract refers;

- when crops are planted or otherwise become growing crops or the young are conceived if the contract is for the sale of unborn young (livestock) to be born within twelve months after contract or for the sale of corps to be harvested within twelve months or the next normal harvest seasons after contracting, whichever is longer.

Thus if Very Fast Food Inc.’s purchasing agent looks at a new type of industrial sponge on Delta Sponge Makers’ store shelf for restaurant supplies, points to it, and says, “I’ll take it,” identification happens then, when the contract is made. But if the purchasing agent wants to purchase sponges for her fast-food restaurants, sees a sample on the shelf, and says, “I want a gross of those”—they come in boxes of one hundred each—identification won’t happen until one or the other of them chooses the gross of boxes of sponges out of the warehouse inventory.

When Title Shifts

Parties May Agree

Assuming identification is done, when does title shift? The law begins with the premise that the agreement of the parties governs. Section 2-401(1) of the UCC says that, in general, “title to goods passes from the seller to the buyer in any manner and on any conditions explicitly agreed on by the parties.” Many companies specify in their written agreements at what moment the title will pass; here, for example, is a clause that appears in sales contracts of Dow Chemical Company: “Title and risk of loss in all goods sold hereunder shall pass to Buyer upon Seller’s delivery to carrier at shipping point.” Thus Dow retains title to its goods only until it takes them to the carrier for transportation to the buyer.

Because the UCC’s default position (further discussed later in this chapter) is that title shifts when the seller has completed delivery obligations, and because the parties may agree on delivery terms, they also may, by choosing those terms, effectively agree when title shifts (again, they also can agree using any other language they want). So it is appropriate to examine some delivery terms at this juncture. There are three possibilities: shipment contracts, destination contracts, and contracts where the goods are not to be moved.

Shipment Contracts

In a shipment contract, the seller’s obligation is to send the goods to the buyer, but not to a particular destination. The typical choices are set out in the UCC at Section 2-319:

- F.O.B. [place of shipment] (the place from which the goods are to be shipped goes in the brackets, as in “F.O.B. Seattle”). F.O.B. means “free on board”; the seller’s obligation, according to Section 2-504 of the UCC, is to put the goods into the possession of a carrier and make a reasonable contract for their transportation, to deliver any necessary documents so the buyer can take possession, and promptly notify the buyer of the shipment.

- F.A.S. [named port] (the name of the seaport from which the ship is carrying the goods goes in the brackets, as in “F.A.S. Long Beach”). F.A.S means “free alongside ship”; the seller’s obligation is to at his “expense and risk deliver the goods alongside the vessel in the manner usual in that port” and to provide the buyer with pickup instructions. Uniform Commercial Code, Section 2-319(2).

- C.I.F. and C. & F. These are actually not abbreviations for delivery terms, but rather they describe who pays insurance and freight. “C.I.F” means “cost, insurance, and freight”—if this term is used, it means that the contract price “includes in a lump sum the cost of the goods and the insurance and freight to the named destination.” Uniform Commercial Code, Section 2-320. “C. & F.” means that “the price so includes cost and freight to the named destination.” Uniform Commercial Code, Section 2-320.

Destination Contracts

In a destination contract, the seller’s obligation is to see to it that the goods actually arrive at the destination. Here again, the parties may employ the use of abbreviations that indicate the seller’s duties. See the following from the UCC, Section 2-319:

- F.O.B. [destination] means the seller’s obligation is to “at his own expense and risk transport the goods to that place and there tender delivery of them” with appropriate pickup instructions to the buyer.

- Ex-ship “is the reverse of the F.A.S. term.” Uniform Commercial Code, Section 2-322. It means “from the carrying vessel”—the seller’s obligation is to make sure the freight bills are paid and that “the goods leave the ship’s tackle or are otherwise properly unloaded.”

- No arrival, no sale means the “seller must properly ship conforming goods and if they arrive by any means he must tender them on arrival but he assumes no obligation that the goods will arrive unless he has caused the non-arrival.” Uniform Commercial Code, Section 2-324. If the goods don’t arrive, or if they are damaged or deteriorated through no fault of the seller, the buyer can either treat the contract as avoided, or pay a reduced amount for the damaged goods, with no further recourse against the seller. Uniform Commercial Code, Section 2-613.

Goods Not to Be Moved

It is not uncommon for contracting parties to sell and buy goods stored in a grain elevator or warehouse without physical movement of the goods. There are two possibilities:

- Goods with documents of title. A first possibility is that the ownership of the goods is manifested by a document of title—“bill of lading, dock warrant, dock receipt, warehouse receipt or order for the delivery of goods, and also any other document which in the regular course of business or financing is treated as adequately evidencing that the person in possession of it is entitled to receive, hold and dispose of the document and the goods it covers.” Uniform Commercial Code, Section 1-201(15). In that case, the UCC, Section 2-401(3)(a), says that title passes “at the time when and the place where” the documents are delivered to the buyer.

- Goods without documents of title. If there is no physical transfer of the goods and no documents to exchange, then UCC, Section 2-401(3)(b), provides that “title passes at the time and place of contracting.”

Here are examples showing how these concepts work.

Suppose the contract calls for Delta Sponge Makers to “ship the entire lot of industrial grade Sponge No. 2 by truck or rail” and that is all that the contract says about shipment. That’s a “shipment contract,” and the UCC, Section 2-401(2)(a), says that title passes to Very Fast Foods at the “time and place of shipment.” At the moment that Delta turns over the 144 cartons of 1,000 sponges each to a trucker— perhaps Easy Rider Trucking comes to pick them up at Delta’s own factory—title has passed to Very Fast Foods.

Suppose the contract calls for Delta to “deliver the sponges on June 10 at the Maple Street warehouse of Very Fast Foods Inc.” This is a destination contract, and the seller “completes his performance with respect to the physical delivery of the goods” when it pulls up to the door of the warehouse and tenders the cartons. Uniform Commercial Code, Section 2-401(2)(b). “Tender” means that the party—here Delta Sponge Makers—is ready, able, and willing to perform and has notified its obligor of its readiness. When the driver of the delivery truck knocks on the warehouse door, announces that the gross of industrial grade Sponge No. 2 is ready for unloading, and asks where the warehouse foreman wants it, Delta has tendered delivery, and title passes to Very Fast Foods.

Suppose Very Fast Foods fears that the price of industrial sponges is about to soar; it wishes to acquire a large quantity long before it can use them all or even store them all. Delta does not store all of its sponges in its own plant, keeping some of them instead at Central Warehousing. Central is a bailee, one who has rightful possession but not title. (A parking garage often is a bailee of its customers’ cars; so is a carrier carrying a customer’s goods.) Now assume that Central has issued a warehouse receipt (a document of title that provides proof of ownership of goods stored in a warehouse) to Delta and that Delta’s contract with Very Fast Foods calls for Delta to deliver “document of title at the office of First Bank” on a particular day. When the goods are not to be physically moved, that title passes to Very Fast Foods “at the time when and the place where” Delta delivers the document.

Suppose the contract did not specify physical transfer or exchange of documents for the purchase price. Instead, it said, “Seller agrees to sell all sponges stored on the north wall of its Orange Street warehouse, namely, the gross of industrial Sponge No. 2, in cartons marked B300–B444, to Buyer for a total purchase price of $14,000, payable in twelve equal monthly installments, beginning on the first of the month beginning after the signing of this agreement.” Then title passes at the time and place of contracting—that is, when Delta Sponge Makers and Very Fast Foods sign the contract.

So, as always under the UCC, the parties may agree on the terms they want when title shifts. They can do that directly by just saying when—as in the Dow Chemical example—or they can indirectly agree when title shifts by stipulating delivery terms: shipment, destination, goods not to be moved. If they don’t stipulate, the UCC default kicks in.

UCC Default Provision

If the parties do not stipulate by any means when title shifts, Section 2-401(2) of the UCC provides that “title passes to the buyer at the time and place at which seller completes his performance with reference to the physical delivery of the goods.” And if the parties have no term in their contract about delivery, the UCC’s default delivery term controls. It says “the place for delivery is the seller’s place of business or if he has none his residence,” and delivery is accomplished at the place when the seller “put[s] and hold[s] conforming goods at the buyer’s disposition and give[s] the buyer any notification reasonably necessary to enable him to take delivery.” Uniform Commercial Code, Sections 2-308 and 2-503.

Title from Nonowners

The Problem of Title from Nonowners

We have examined when title transfers from buyer to seller, and here the assumption is, of course, that seller had good title in the first place. But what title does a purchaser acquire when the seller has no title or has at best only a voidable title? This question has often been difficult for courts to resolve. It typically involves a type of eternal triangle with a three-step sequence of events, as follows (see Figure 18.1 “Sales by Nonowners”): (1) The nonowner obtains possession, for example, by loan or theft; (2) the nonowner sells the goods to an innocent purchaser for cash; and (3) the nonowner then takes the money and disappears, goes into bankruptcy, or ends up in jail. The result is that two innocent parties battle over the goods, the owner usually claiming that the purchaser is guilty of conversion (i.e., the unlawful assumption of ownership of property belonging to another) and claiming damages or the right to recover the goods.

Figure 18.1 Sales by Nonowners

The Response to the Problem of Title from Nonowners The Basic Rule

To resolve this dilemma, we begin with a basic policy of jurisprudence: a person cannot transfer better title than he or she had. (The Uniform Commercial Code notes this policy in Sections 2-403, 2A- 304, and 2A-305.) This policy would apply in a sale-of-goods case in which the nonowner had a void title or no title at all. For example, if a nonowner stole the goods from the owner and then sold them to an innocent purchaser, the owner would be entitled to the goods or to damages. Because the thief had no title, he had no title to transfer to the purchaser. A person cannot get good title to goods from a thief, nor does a person have to retain physical possession of her goods at all times to retain their ownership—people are expected to leave their cars with a mechanic for repair or to leave their clothing with a dry cleaner.

If thieves could pass on good title to stolen goods, there would be a hugely increased traffic in stolen property; that would be unacceptable. In such a case, the owner can get her property back from whomever the thief sold it to in an action called replevin (an action to recover personal property unlawfully taken). On the other hand, when a buyer in good faith buys goods from an apparently reputable seller, she reasonably expects to get good title, and that expectation cannot be dashed with impunity without faith in the market being undermined. Therefore, as between two innocent parties, sometimes the original owner does lose, on the theory that (1) that person is better able to avoid the problem than the downstream buyer, who had absolutely no control over the situation, and (2) faith in commercial transactions would be undermined by allowing original owners to claw back their property under all circumstances.

So the basic legal policy that a person cannot pass on better title than he had is subject to a number of exceptions. Likewise, the law governing the sale of goods contains exceptions to the basic legal policy. These usually fall within one of two categories: sellers with voidable title and entrustment.

The Exceptions

As noted, there are exceptions to the law governing the sale of goods.

Sellers with a Voidable Title

Under the UCC, a person with a voidable title has the power to transfer title to a good-faith purchaser for value (see Figure 18.2 “Voidable Title”). The UCC defines good faith as “honesty in fact in the conduct or transaction concerned.” Uniform Commercial Code, Section 1-201(19). A “purchaser” is not restricted to one who pays cash; any taking that creates an interest in property, whether by mortgage, pledge, lien, or even gift, is a purchase for purposes of the UCC. And “value” is not limited to cash or goods; a person gives value if he gives any consideration sufficient to support a simple contract, including a binding commitment to extend credit and security for a preexisting claim. Recall from the section in Contract Law on “The Agreement” that a “voidable” title is one that, for policy reasons, the courts will cancel on application of one who is aggrieved. These reasons include fraud, undue influence, mistake, and lack of capacity to contract. When a person has a voidable title, title can be taken away from her, but if it is not, she can transfer better title than she has to a good-faith purchaser for value.

Rita, sixteen years old, sells a video game to her neighbor Annie, who plans to give the game to her nephew. Since Rita is a minor, she could rescind the contract; that is, the title that Annie gets is voidable: it is subject to be avoided by Rita’s rescission. But Rita does not rescind. Then Annie discovers that her nephew already has that video game, so she sells it instead to an office colleague, Donald. He has had no notice that Annie bought the game from a minor and has only a voidable title. He pays cash. Should Rita— the minor—subsequently decide she wants the game back, it would be too late: Annie has transferred good title to Donald even though Annie’s title was voidable.

Figure 18.2 Voidable Title

Suppose Rita was an adult and Annie paid her with a check that later bounced, but Annie sold the game to Donald before the check bounced. Does Donald still have good title? The UCC says he does, and it identifies three other situations in which the good-faith purchaser is protected: (1) when the original transferor was deceived about the identity of the purchaser to whom he sold the goods, who then transfers to a good-faith purchaser; (2) when the original transferor was supposed to but did not receive cash from the intermediate purchaser; and (3) when “the delivery was procured through fraud punishable as larcenous under the criminal law.” Uniform Commercial Code, Sections 2-403(1), 2-403(1), 2A-304, and 2A-305.

This last situation may be illustrated as follows: Dimension LLC leased a Volkswagen to DK Inc. The agreement specified that DK could use the Volkswagen solely for business and commercial purposes and could not sell it. Six months later, the owner of DK, Darrell Kempf, representing that the Volkswagen was part of DK’s used-car inventory, sold it to Edward Seabold. Kempf embezzled the proceeds from the sale of the car and disappeared. When DK defaulted on its payments for the Volkswagen, Dimension attempted to repossess it. Dimension discovered that Kempf had executed a release of interest on the car’s title by forging the signature of Dimension’s manager. The Washington Court of Appeals, applying the UCC, held that Mr. Seabold should keep the car. The car was not stolen from Dimension; instead, by leasing the vehicle to DK, Dimension transferred possession of the car to DK voluntarily, and because Seabold was a good-faith purchaser, he won. Dimension Funding, L.L.C. v. D.K. Associates, Inc., 191 P.3d 923 (Wash. App. 2008).

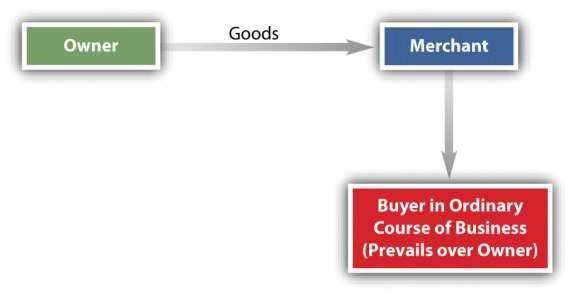

Entrustment

A merchant who deals in particular goods has the power to transfer all rights of one who entrusts to him goods of the kind to a “buyer in the ordinary course of business” (see Figure 18.3 “Entrustment”). Uniform Commercial Code, Sections 2-403(2), 2A-304(2), and 2A-305(2). The UCC defines such a buyer as a person who buys goods in an ordinary transaction from a person in the business of selling that type of goods, as long as the buyer purchases in “good faith and without knowledge that the sale to him is in violation of the ownership rights or security interest of a third party in the goods.” Uniform Commercial Code, Section 1-201(9). Bess takes a pearl necklace, a family heirloom, to Wellborn’s Jewelers for cleaning; as the entrustor, she has entrusted the necklace to an entrustee. The owner of Wellborn’s—perhaps by mistake—sells it to Clara, a buyer, in the ordinary course of business. Bess cannot take the necklace back from Clara, although she has a cause of action against Wellborn’s for conversion. As between the two innocent parties, Bess and Clara (owner and purchaser), the latter prevails. Notice that the UCC only says that the entrustee can pass whatever title the entrustor had to a good-faith purchaser, not necessarily good title. If Bess’s cleaning woman borrowed the necklace, soiled it, and took it to Wellborn’s, which then sold it to Clara, Bess could get it back because the cleaning woman had no title to transfer to the entrustee, Wellborn’s.

Figure 18.3 Entrustment

Entrustment is based on the general principle of estoppel: “A rightful owner may be estopped by his own acts from asserting his title. If he has invested another with the usual evidence of title, or an apparent authority to dispose of it, he will not be allowed to make claim against an innocent purchaser dealing on the faith of such apparent ownership.” Zendman v. Harry Winston, Inc., 111 N.E. 2d 871 (N.Y. 1953).

Risk of Loss

Why Risk of Loss Is Important

“Risk of loss” means who has to pay—who bears the risk—if the goods are lost or destroyed without the fault of either party. It is obvious why this issue is important: Buyer contracts to purchase a new car for $35,000. While the car is in transit to Buyer, it is destroyed in a landslide. Who takes the $35,000 hit? The CISG, Article 66, provides as follows: “Loss of or damage to the goods after the risk has passed to the buyer does not discharge him from his obligation to pay the price, unless the loss or damage is due to an act or omission of the seller.”

When Risk of Loss Passes

The Parties May Agree

Just as title passes in accordance with the parties’ agreement, so too can the parties fix the risk of loss on one or the other. They may even devise a formula to divide the risk between themselves. Uniform Commercial Code, Section 2-303.

Common terms by which parties set out their delivery obligations that then affect when title shifts (F.O.B., F.A.S., ex-ship, and so on) were discussed earlier in this chapter. Similarly, parties may use common terms to set out which party has the risk of loss; these situation arise with trial sales. That is, sometimes the seller will permit the buyer to return the goods even though the seller had conformed to the contract. When the goods are intended primarily for the buyer’s use, the transaction is said to be “sale on approval.” When they are intended primarily for resale, the transaction is said to be “sale or return.” When the “buyer” is really only a sales agent for the “seller,” it is a consignment sale.

Sale on Approval

Under a sale-on-approval contract, risk of loss (and title) remains with the seller until the buyer accepts, and the buyer’s trial use of the goods does not in itself constitute acceptance. If the buyer decides to return the goods, the seller bears the risk and expense of return, but a merchant buyer must follow any reasonable instructions from the seller. Very Fast Foods asks Delta for some sample sponges to test on approval; Delta sends a box of one hundred sponges. Very Fast plans to try them for a week, but before that, through no fault of Very Fast, the sponges are destroyed in a fire. Delta bears the loss. Uniform Commercial Code, Section 2-327(1)(a).

Sale or Return

The buyer might take the goods with the expectation of reselling them—as would a women’s wear shop buy new spring fashions, expecting to sell them. But if the shop doesn’t sell them before summer wear is in vogue, it could arrange with the seller to return them for credit. In contrast to sale-on-approval contracts, sale-or-return contracts have risk of loss (and title too) passing to the buyer, and the buyer bears the risk and expense of returning the goods. Occasionally the question arises whether the buyer’s other creditors may claim the goods when the sales contract lets the buyer retain some rights to return the goods. The answer seems straightforward: in a sale-on-approval contract, where title remains with the seller until acceptance, the buyer does not own the goods—hence they cannot be seized by his creditors—unless he accepts them, whereas they are the buyer’s goods (subject to his right to return them) in a sale-or-return contract and may be taken by creditors if they are in his possession.

Consignment Sales

In a consignment situation, the seller is a bailee and an agent for the owner who sells the goods for the owner and takes a commission. Under the Uniform Commercial Code (UCC), this is considered a sale or return, thus the consignee (at whose place the goods are displayed for sale to customers) is considered a buyer and has the risk of loss and title. Uniform Commercial Code, Section 2-326(3). The consignee’s creditors can take the goods; that is, unless the parties comply “with an applicable law providing for a consignor’s interest or the like to be evidenced by a sign, or where it is established that the person conducting the business is generally known by his creditors to be substantially engaged in selling the goods of others” (or complies with secured transactions requirements under Article 9, discussed in a later chapter). Uniform Commerical Code, Section 2-326.

The UCC Default Position

If the parties fail to specify how the risk of loss is to be allocated or apportioned, the UCC again supplies the answers. A generally applicable rule, though not explicitly stated, is that risk of loss passes when the seller has completed obligations under the contract. Notice this is not the same as when title passes: title passes when seller has completed delivery obligations under the contract, risk of loss passes when all obligations are completed. (Thus a buyer could get good title to nonconforming goods, which might be better for the buyer than not getting title to them: if the seller goes bankrupt, at least the buyer has something of value.)

Risk of Loss in Absence of a Breach

If the goods are conforming, then risk of loss would indeed pass when delivery obligations are complete, just as with title. And the analysis here would be the same as we looked at in examining shift of title.

A shipment contract. The contract requires Delta to ship the sponges by carrier but does not require it to deliver them to a particular destination. In this situation, risk of loss passes to Very Fast Foods when the goods are delivered to the carrier.

The CISG—pretty much like the UCC—provides as follows (Article 67):

If the contract of sale involves carriage of the goods and the seller is not bound to hand them over at a particular place, the risk passes to the buyer when the goods are handed over to the first carrier for transmission to the buyer in accordance with the contract of sale. If the seller is bound to hand the goods over to a carrier at a particular place, the risk does not pass to the buyer until the goods are handed over to the carrier at that place.

A destination contract. If the destination contract agreement calls for Delta to deliver the sponges by carrier to a particular location, Very Fast Foods assumes the risk of loss only when Delta’s carrier tenders them at the specified place.

The CISG provides for basically the same thing (Article 69): “If the contract is for something other than shipment, the risk passes to the buyer when he takes over the goods or, if he does not do so in due time, from the time when the goods are placed at his disposal and he commits a breach of contract by failing to take delivery.”

Goods not to be moved. If Delta sells sponges that are stored at Central Warehousing to Very Fast Foods, and the sponges are not to be moved, Section 2-509(2) of the UCC sets forth three possibilities for transfer of the risk of loss:

- The buyer receives a negotiable document of title covering the good. A document of title is negotiable if by its terms goods are to be delivered to the bearer of the document or to the order of a named person.

- The bailee acknowledges the buyer’s right to take possession of the goods. Delta signs the contract for the sale of sponges and calls Central to inform it that a buyer has purchased 144 cartons and to ask it to set aside all cartons on the north wall for that purpose. Central does so, sending notice to Very Fast Foods that the goods are available. Very Fast Foods assumes risk of loss upon receipt of the notice.

- When the seller gives the buyer a nonnegotiable document of title or a written direction to the bailee to deliver the goods and the buyer has had a reasonable time to present the document or direction.

All other cases. In any case that does not fit within the rules just described, the risk of loss passes to the buyer only when the buyer actually receives the goods. Cases that come within this section generally involve a buyer who is taking physical delivery from the seller’s premises. A merchant who sells on those terms can be expected to insure his interest in any goods that remain under his control. The buyer is unlikely to insure goods not in his possession. The case of Ramos v. Wheel Sports Center, 409 N.Y.S.2d 505 (N.Y. Civ. Ct. 1978) demonstrates how this risk-of-loss provision applies when a customer pays for merchandise but never actually receives his purchase because of a mishap. “Whether the contract involves delivery at the seller’s place of business or at the situs of the goods, a merchant seller cannot transfer risk of loss and it remains on him until actual receipt by the buyer, even though full payment has been made and the buyer notified that the goods are at his disposal. The underlying theory is that a merchant who is to make physical delivery at his own place continues meanwhile to control the goods and can be expected to insure his interest in them.” Ramos v. Wheel Sports Center, 409 N.Y.S.2d 505 (N.Y. Civ. Ct. 1978)

Risk of Loss Where Breach Occurs

The general rule for risk of loss was set out as this: risk of loss shifts when seller has completed obligations under the contract. We said if the goods are conforming, the only obligation left is delivery, so then risk of loss would shift upon delivery. But if the goods are nonconforming, then the rule would say the risk doesn’t shift. And that’s correct, though it’s subject to one wrinkle having to do with insurance. Let’s examine the two possible circumstances: breach by seller and breach by buyer.

First, suppose the seller breaches the contract by proffering nonconforming goods, and the buyer rejects them—never takes them at all. Then the goods are lost or damaged. Under Section 2-510(1) of the UCC, the loss falls on seller and remains there until seller cures the breach or until buyer accepts despite the breach. Suppose Delta is obligated to deliver a gross of industrial No. 2 sponges; instead it tenders only one hundred cartons or delivers a gross of industrial No. 3 sponges. The risk of loss falls on Delta because Delta has not completed its obligation under the contract and Very Fast Foods doesn’t have possession of the goods. Or suppose Delta has breached the contract by tendering to Very Fast Foods a defective document of title. Delta cures the defect and gives the new document of title to Very Fast Foods, but before it does so the sponges are stolen. Delta is responsible for the loss.

Now suppose that a seller breaches the contract by proffering nonconforming goods and that the buyer, not having discovered the nonconformity, accepts them—the nonconforming goods are in the buyer’s hands. The buyer has a right to revoke acceptance, but before the defective goods are returned to the seller, they are destroyed while in the buyer’s possession. The seller breached, but here’s the wrinkle: the UCC says that the seller bears the loss only to the extent of any deficiency in the buyer’s insurance coverage. Uniform Commercial Code, Section 2-510(2). Very Fast Foods had taken delivery of the sponges and only a few days later discovered that the sponges did not conform to the contract. Very Fast has the right to revoke and announces its intention to do so. A day later its warehouse burns down and the sponges are destroyed. It then discovers that its insurance was not adequate to cover all the sponges. Who stands the loss? The seller does, again, to the extent of any deficiency in the buyer’s insurance coverage.

Second, what if the buyer breaches the contract? Here’s the scenario: Suppose Very Fast Foods calls two days before the sponges identified to the contract are to be delivered by Delta and says, “Don’t bother; we no longer have a need for them.” Subsequently, while the lawyers are arguing, Delta’s warehouse burns down and the sponges are destroyed. Under the rules, risk of loss does not pass to the buyer until the seller has delivered, which has not occurred in this case. Nevertheless, responsibility for the loss here has passed to Very Fast Foods, to the extent that the seller’s insurance does not cover it. Section 2-510(3) of the UCC permits the seller to treat the risk of loss as resting on the buyer for a “commercially reasonable time” when the buyer repudiates the contract before risk of loss has passed to him. This transfer of the risk can take place only when the goods are identified to the contract. The theory is that if the buyer had taken the goods as per the contract, the goods would not have been in the warehouse and thus would not have been burned up.

Insurable Interest

Why It Matters

We noted at the start of this chapter that who has title is important for several reasons, one of which is because it affects who has an insurable interest. (You can’t take out insurance in something you have no interest in: if you have no title, you may not have an insurable interest.) And it was noted that the rules on risk of loss are affected by insurance. (The theory is that a businessperson is likely to have insurance, which is a cost of business, and if she has insurance and also has possession of goods—even nonconforming ones—it is reasonable to charge her insurance with loss of the goods; thus she will have cause to take care of them in her possession, else her insurance rates increase.) So in commercial transactions insurance is important, and when goods are lost or destroyed, the frequent argument is between the buyer’s and the seller’s insurance companies, neither of which wants to be responsible. They want to deny that their insured had an insurable interest. Thus it becomes important who has an insurable interest.

Insurable Interest of the Buyer

It is not necessary for the buyer to go all the way to having title in order for him to have an insurable interest. The buyer obtains a “special property and insurable interest in goods by identification of existing goods as goods to which the contract refers.” Uniform Commercial Code, Section 2-501(1). We already discussed how “identification” of the goods can occur. The parties can do it by branding, marking, tagging, or segregating them—and they can do it at any time. We also set out the rules for when goods will be considered identified to the contract under the UCC if the parties don’t do it themselves.

Insurable Interest of the Seller

As long as the seller retains title to or any security interest in the goods, he has an insurable interest.

Other Rights of the Buyer

The buyer’s “special property” interest that arises upon identification of goods gives the buyer rights other than that to insure the goods. For example, under Section 2-502 of the UCC, the buyer who has paid for unshipped goods may take them from a seller who becomes insolvent within ten days after receipt of the whole payment or the first installment payment. Similarly, a buyer who has not yet taken delivery may sue a third party who has in some manner damaged the property.

CC license: Attribution-NonCommercial-ShareAlike 3.0 Unported (CC BY-NC-SA 3.0)- Saylor.org